Last week CBO released its annual summer update of its budget and economic outlook. Yesterday’s blog posting discussed one aspect of that outlook—the amount of discretionary spending that will occur over the coming decade under current law. Today we’ll summarize the estimated impact of fiscal policy on near-term economic growth (which is discussed on pages 37 to 39 of the report).

Under current law, federal fiscal policy—including the effects of both legislative actions and automatic changes in the budget—will provide decreasing support for economic activity this year and significantly restrain economic growth in calendar years 2012 and 2013. One reason for that pattern is that the stimulative impact of the American Recovery and Reinvestment Act (ARRA) is winding down. CBO estimates that relative to what would have happened without that law, ARRA raised real GDP by between 1.5 percent and 4.2 percent in 2010 but will increase GDP by between 0.8 percent and 2.3 percent in 2011 and by between 0.3 percent and 0.8 percent in 2012. ARRA’s boost to employment is also diminishing. CBO estimates that the law raised employment (relative to what it would have been otherwise) by between 1.3 million and 3.3 million people in 2010, but the law’s impact on employment is projected to be progressively smaller in 2011 and 2012. (For a discussion of CBO’s estimation methods and evidence on the economic effects of fiscal stimulus, see the report Estimated Impact of the American Recovery and Reinvestment Act on Employment and Economic Output from April 2011 Through June 2011.)

Another reason for the decrease in economic support from fiscal policy is that the effect of the government’s so-called automatic fiscal stabilizers is declining as the economy continues to grow (albeit slowly). Those stabilizers are the automatic responses of revenues and outlays to cyclical movements in real GDP and unemployment. For example, when GDP falls relative to potential GDP during a recession, the reduction in income causes tax revenues to decrease automatically. In addition, some outlays—such as for unemployment insurance and federal nutrition benefits—automatically increase. Those automatic responses provide fiscal support when economic activity slows and provide fiscal restraint when economic activity picks up.

The economic support provided by federal fiscal policy will also diminish as provisions of the 2010 tax act expire as scheduled over the next two years and as the Budget Control Act is implemented:

- The 2010 tax act extended numerous tax cuts that were slated to expire at the end of 2010; for example, it continued through 2012 various tax reductions enacted in 2001 and 2003, and it extended through 2011 provisions limiting the reach of the alternative minimum tax (AMT). It also reduced the employee’s share of the Social Security payroll tax in 2011, provided temporary tax incentives for business investment, and extended certain additional unemployment insurance benefits.

- The Budget Control Act set caps on discretionary spending that will reduce such spending in real terms over time. It also created a special Congressional committee on deficit reduction. If, by January 15, 2012, legislation originating from that committee and projected to achieve at least $1.2 trillion in savings over the next 10 years is not enacted, automatic procedures established by the new law will reduce spending between fiscal years 2013 and 2021 by the difference between $1.2 trillion and any savings that are achieved by enacting proposals from the committee. That spending reduction (with an allowance for interest savings subtracted) would be distributed evenly among those fiscal years. Because CBO cannot predict what legislation from the deficit reduction committee might be enacted, the agency’s economic forecast is based on the amounts of the automatic spending reductions (an estimated $111 billion per year), which would have their biggest effect on the growth of GDP in 2013, when they first take effect.

CBO estimates that the fiscal restraint stemming from the expiration of provisions in the 2010 tax act and from enactment of the Budget Control Act will decrease real GDP in calendar year 2013 by between about 1½ percent and about 3½ percent compared with what it would have been otherwise. However, CBO also estimates that the reduction in deficits resulting from those policies will boost output later in the decade. (To reflect the high degree of uncertainty that accompanies estimates of the economic impact of fiscal policy, CBO used a range of assumptions about the extent to which changes in taxes and government spending affect the demand for goods and services, budget deficits affect private investment, and changes in marginal tax rates on labor income affect the labor supply. For more information about those assumptions and CBO’s methodology for producing such estimates, see our analysis of The Macroeconomic and Budgetary Effects of an Illustrative Policy for Reducing the Federal Budget Deficit and our recent letter on the effects of government spending on economic growth.)

Future fiscal policy is likely to differ from that embodied in current law in at least some respects. For example, the Congress might enact legislation from the deficit reduction committee that includes a different timing or composition of policy changes than CBO has assumed on the basis of the amounts of the automatic spending cuts, or the Congress might alter fiscal policy in other ways.

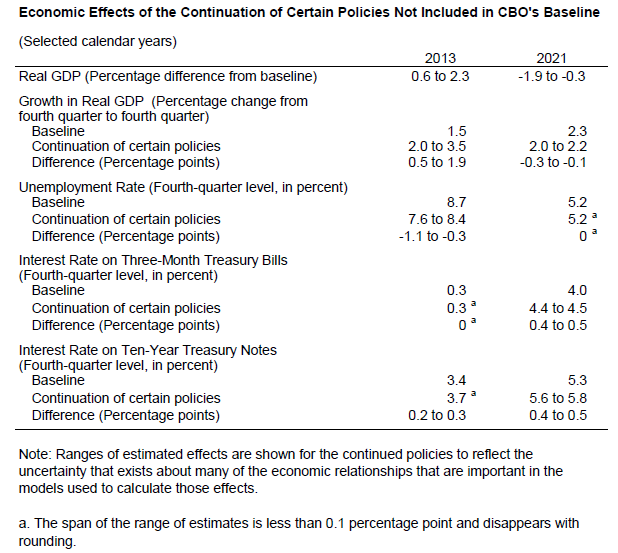

To illustrate how some widely anticipated changes to current law would affect the economy, CBO has examined an alternative path for fiscal policy that includes the following assumptions: Most of the cuts in individual income taxes and estate and gift taxes now scheduled to expire in 2012 or 2013 are extended through 2021; limits to the reach of the AMT that are set to expire at the end of 2011 are also continued through 2021; and Medicare’s payment rates for physicians are maintained at their 2011 levels. (Those possible changes to current law would be a continuation of current policies that have previously been extended; they do not represent a prediction or recommendation about future policies.) Under that set of policies, budget deficits would be significantly larger than in CBO’s baseline budget projections, and federal debt held by the public would accumulate much more rapidly.

Under those alternative assumptions, real GDP would be higher in the first few years of the projection period than in CBO’s baseline economic forecast (see the table below). For example, CBO estimates that the size of real GDP in calendar year 2013 would be between 0.6 percent and 2.3 percent greater than projected under current law. Stronger GDP would result in a lower unemployment rate and somewhat higher interest rates over the next few years. In later years, however, real GDP would fall below the level in CBO’s baseline projection by increasing amounts over time. The lower marginal tax rates under those alternative assumptions would increase people’s incentives to work and save, but the larger budget deficits would reduce (“crowd out”) private investment in productive capital. By the end of 2021, as the effect of larger budget deficits outweighed that of lower tax rates, real GDP would be between 0.3 percent and 1.9 percent smaller than it would be under current law, CBO estimates. In years beyond 2021, the effects would become even larger.