Choices for Deficit Reduction

Are fiscal rules a useful tool for achieving budgetary goals? View the appendix of this report to learn more.

Summary

An update to this report, Choices for Deficit Reduction: An Update was published in December 2013

This report reviews the magnitude and causes of the federal government’s budgetary imbalance, various options for bringing spending and taxes into closer alignment, and criteria that lawmakers and the public might use to evaluate different approaches to deficit reduction.

How Big Are Projected U.S. Deficits and Debt?

Federal debt held by the public currently exceeds 70 percent of the nation’s annual output (gross domestic product, or GDP), a percentage not seen since 1950. Under the current-law assumptions embodied in CBO’s baseline projections, the budget deficit would shrink markedly—from nearly $1.1 trillion in fiscal year 2012 to about $200 billion in 2022—and debt would decline to 58 percent of GDP in 2022. However, those projections depend heavily on the significant increases in taxes and decreases in spending that are scheduled to take effect at the beginning of January.

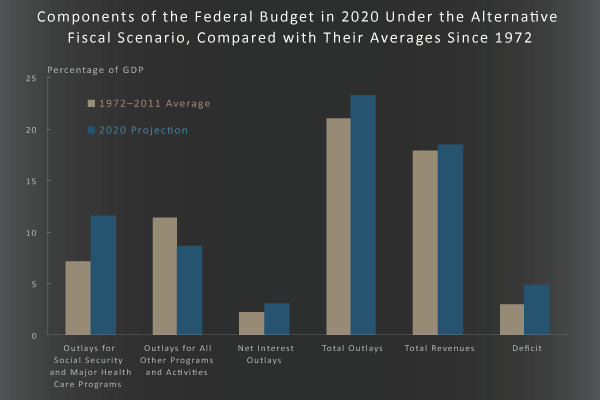

If, instead, lawmakers maintained current policies by preventing most of those changes from occurring—what CBO refers to as the alternative fiscal scenario—annual deficits would average nearly 5 percent of GDP over the next decade, and debt held by the public would increase to 90 percent of GDP 10 years from now and keep rising rapidly thereafter.

What Factors Are Putting Increasing Pressure on the Budget?

The aging of the baby-boom generation portends a significant and sustained increase in coming years in the share of the population that will receive benefits from Social Security and Medicare and long-term care services financed through Medicaid. Moreover, per capita spending on health care is likely to continue to grow faster than per capita spending on other goods and services for many years. Without significant changes in the laws governing Social Security, Medicare, and Medicaid, those factors will boost federal outlays as a percentage of GDP well above the average of the past four decades—a conclusion that applies under any plausible assumptions about future trends in demographics, economic conditions, and health care costs (see figure below).

What Are the Consequences of Rising Federal Debt?

Prolonged increases in debt relative to GDP can cause significant long-term damage to both the government’s finances and the broader economy. Such increases in federal debt would have the following consequences:

- Higher federal spending on interest payments;

- A reduction in national saving;

- Limits on policymakers’ ability to use tax and spending policies to respond to unexpected challenges, such as economic downturns, natural disasters, or financial crises; and

- An increase in the likelihood of a fiscal crisis, in which investors would lose confidence in the government’s ability to manage its budget, and the government would thus lose the ability to borrow at affordable interest rates.

What Are Some Possible Targets for Deficit Reduction?

Making policy changes that are large enough to shrink the debt relative to the size of the economy—or even to keep the debt from growing—will be a formidable task. For simplicity, this report focuses on potential deficit reduction in one year: 2020. It concentrates on CBO’s alternative fiscal scenario, rather than on the current-law baseline, to show the size of the policy changes—relative to policies now in place—that would be necessary to put the budget on a more sustainable path.

Lawmakers could set various deficit reduction goals for 2020, such as the following:

| Approximate Amount of Deficit Reduction in 2020 (Relative to the alternative fiscal scenario and excluding interest savings) |

Impact on Budgetary Outcomes |

| $1 Trillion | The budget would be balanced by 2020; debt would be on a steadily declining path relative to GDP. |

| $750 Billion | Deficts would be similar to those projected in the current-law baseline (equaling a small percentage of GDP each year), and debt would be on a slightly downward-sloping path relative to GDP. |

| $500 Billion | Debt would be about the same percentage of GDP at the end of 2020 that it will be early in 2013 under the alternative fiscal scenario (about 75 percent). |

What Kinds of Policy Changes Could Lead to a More Sustainable Budgetary Path?

The report lists a number of options, mostly taken from previous CBO publications, that illustrate how challenging it would be to shrink the deficit in 2020 by any of the amounts shown above, relative to the shortfalls projected under current policies. The options—some of which would increase revenues and others of which would reduce spending—are meant to be illustrative only; many other possible policy changes could be considered.

Very few of the policy changes that CBO has examined in the past are large enough, by themselves, to accomplish a sizable portion of the deficit reduction necessary to put the budget on a more sustainable path. In addition, many of the options that would have a substantial budgetary impact would require large numbers of people to pay more in taxes or receive less in government benefits or services.

For example, it is possible to keep tax revenues at their historical average percentage of GDP—but only by making substantial cuts, relative to current policies, in the large benefit programs that aid a broad group of people at some point in their lives. Alternatively, it is possible to keep the policies for those large benefit programs unchanged—but only by raising taxes substantially, relative to current policies, for a broad segment of the population. Changes in other federal programs can affect the size of the changes needed in taxes or large benefit programs, but they cannot eliminate the basic trade-off between those two parts of the budget. Ultimately, significant deficit reduction is likely to require a combination of policies, many of which may stand in stark contrast to policies now in place.

What Criteria Might Be Used to Evaluate Policy Changes?

In considering policy changes that would reduce budget deficits, lawmakers and the public may weigh several factors. The types of changes that people will be willing to accept will depend in part on their view of the proper size of the federal government and the best allocation of its resources. People may also want to consider the distributional implications of proposed changes—that is, who would bear the burden of particular cuts in spending or increases in taxes and who would realize any long-term economic benefits. In addition, some policy changes would have a large and immediate impact on the budget, whereas others would have effects that would grow considerably over time.

A related consideration is how policy changes would influence the pace of economic recovery and longer-term economic performance. Lawmakers face difficult trade-offs in deciding how quickly to implement policies to reduce budget deficits. For example, CBO projects that the significant tax increases and spending cuts that are due to occur in January will probably cause the economy to fall back into a recession next year, but they will make the economy stronger later in the decade and beyond. In contrast, continuing current policies would lead to faster economic growth in the near term but a weaker economy in later years. Potential policy changes would have different effects on federal borrowing, people’s incentives to work and save, and government investment, all of which would affect the nation’s output and income during the next few years and over the longer term.

Updated November 9, 2012, to correct errors in the placement and wording of footnotes in table 4.