Rising Demand for Long-Term Services and Supports for Elderly People

By 2050, one-fifth of the U.S. population will be age 65 or older, up from 12 percent in 2000 and 8 percent in 1950. As a result, expenditures on long-term services and supports for the elderly will rise substantially in the coming decades.

Summary

By 2050, one-fifth of the total U.S. population will be elderly (that is, 65 or older), up from 12 percent in 2000 and 8 percent in 1950. The number of people age 85 or older will grow the fastest over the next few decades, constituting 4 percent of the population by 2050, or 10 times its share in 1950. That growth in the elderly population will bring a corresponding surge in the number of elderly people with functional and cognitive limitations. Functional limitations are physical problems that limit a person’s ability to perform routine daily activities, such as eating, bathing, dressing, paying bills, and preparing meals. Cognitive limitations are losses in mental acuity that may also restrict a person’s ability to perform such activities. On average, about one-third of people age 65 or older report functional limitations of one kind or another; among people age 85 or older, about two-thirds report functional limitations. One study estimates that more than two-thirds of 65-year-olds will need assistance to deal with a loss in functioning at some point during their remaining years of life. If those rates of prevalence continue, the number of elderly people with functional or cognitive limitations, and thus the need for assistance, will increase sharply in coming decades.

What Are Long-Term Services and Supports and Where Do People Receive Them?

The term long-term services and supports (LTSS) refers to the types of assistance provided to people with functional or cognitive limitations to help them perform routine daily activities.

That assistance is provided in several different forms and venues. About 80 percent of elderly people receiving such care live in the community; the remaining 20 percent obtain assistance in institutional settings. Of those living in the community, a small number live in residential communities catering to the needs of elderly people, but most, including many reporting three or more functional limitations, live in private homes. In the community, elderly people with functional limitations receive assistance primarily from family members and friends (generally unpaid and referred to as informal care); they may also pay for assistance (so-called formal care) from long-term care workers, such as home health aides. In contrast, elderly people with severe functional and cognitive limitations, who may require around-the-clock assistance, often live in institutional settings.

According to data from the Medicare Current Beneficiary Survey, or MCBS, the elderly nursing home population has declined over the past 10 years; more elderly people are living in residential care facilities and other types of care facilities, in community-based housing with supportive services, and in houses in a regular community with no supportive services. That trend is especially pronounced for people 85 or older.

How Are Long-Term Services and Supports Financed?

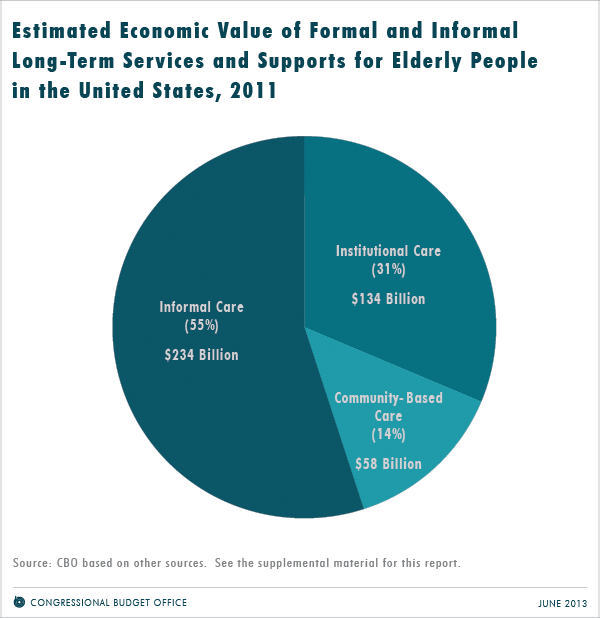

Long-term services and supports are provided and paid for both privately and publicly. More than half of that care is donated—as informal care—by family members and friends, most commonly by spouses and adult daughters. Providing care imposes costs on informal caregivers in the form of time, effort, forgone wages, and other economic costs. Assuming that informal caregivers provide care similar in value to that provided by home health aides, CBO estimates that the value of that care totaled approximately $234 billion in 2011 (see figure below). Because many informal caregivers must sacrifice time that might otherwise be spent earning a wage, the value of that care in terms of forgone wages could be even higher.

The economic value of informal care is substantially higher than total payments for LTSS, which reached about $192 billion in 2011. The largest payers for LTSS, accounting for about two-thirds of total spending, are the major government health care programs, Medicaid and Medicare (see figure below). Out-of-pocket spending is the biggest source of private spending for LTSS and is particularly large for institutional care. Private insurance pays for only a small share of total spending on LTSS, although the number of people with private long-term care (LTC) insurance is growing slowly. Other sources of payment include various federal and state programs for elderly people and private charitable donations.

Many, if not most, people do not make private financial preparations for their future LTSS needs. They may not have the personal financial resources necessary to purchase private LTC insurance, their health history may preclude the possibility of obtaining such insurance, or they may have concerns about the value of private coverage, including uncertainty about the stability of premiums in the future and the ability of insurance carriers to pay for care that might not be needed for several more decades. Other people may prefer to spend their money on activities while they are still healthy, expecting that their quality of life if they are severely impaired would not be much better even if they had more money to spend on assistive services. Some people may mistakenly expect that their private health insurance (not long-term care insurance) or Medicare will provide for their needs or that they will be able to easily obtain Medicaid coverage. Some research finds that the availability of Medicaid deters some people from purchasing private coverage, even though Medicaid is an imperfect substitute for private insurance. Other people may believe that their income and savings will be sufficient or that they will be able to obtain the assistance they need from family members and close friends.

How Might Expenditures on Long-Term Services and Supports Change Over Time?

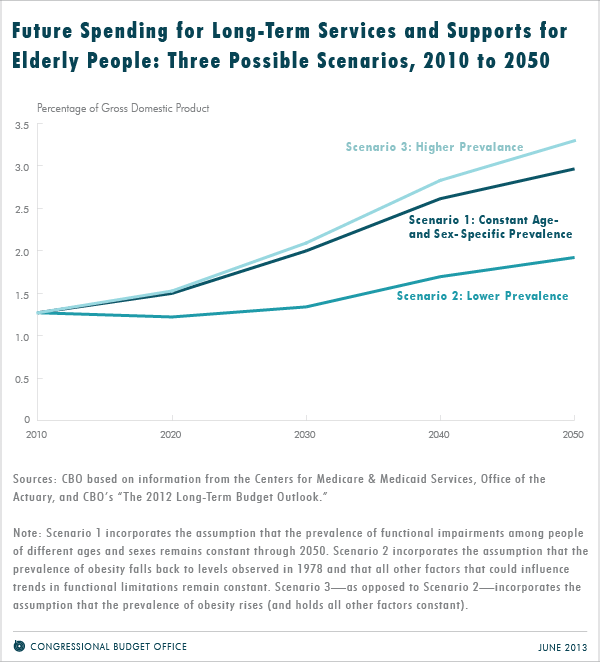

LTSS expenditures for elderly people now account for an estimated 1.3 percent of gross domestic product (GDP). That share is likely to rise in the future as the population ages. To explore the potential implications of the growing elderly population, CBO developed three alternative scenarios regarding the future prevalence of functional limitations among the elderly, holding constant other factors affecting those expenditures, such as growth in prices for LTSS, changes in family structure that could affect the provision of informal care, and changes in how services and supports are delivered. In those scenarios, LTSS expenditures were projected to range from 1.9 percent of GDP to 3.3 percent of GDP by 2050. (The combination of actual future prevalence of functional limitations and changes in those other factors could result in LTSS spending that was less than 1.9 percent of GDP or more than 3.3 percent of GDP by 2050 (see figure below). Spending could be higher, for example, if the provision of informal care fell relative to the provision of formal care as a result of a shrinking average family size.)

Projections of LTSS expenditures are subject to considerable uncertainty. In addition to estimates of the prevalence of functional limitations, they require judgments about future innovations in the delivery of care, changes in the use of services, and future rates of growth in the costs of labor and other inputs to long-term care.