An Update to the Budget and Economic Outlook: 2014 to 2024

The deficit this year will be $506 billion, CBO estimates, about $170 billion lower than the deficit in 2013. After a weak first half of this year, CBO expects economic growth to pick up and the unemployment rate to continue to fall.

Summary

The federal budget deficit has fallen sharply during the past few years, and it is on a path to decline further this year and next year. However, later in the coming decade, if current laws governing federal taxes and spending generally remained unchanged, revenues would grow only slightly faster than the economy and spending would increase more rapidly, according to CBO's projections. Consequently, relative to the size of the economy, deficits would grow and federal debt would climb.

CBO's budget projections are built upon its economic forecast, which anticipates that the economy will grow slowly this year, on balance, and then at a faster but still moderate pace over the next few years. The gap between the nation's output and its potential (maximum sustainable) output will narrow to its historical average by the end of 2017, CBO expects, largely eliminating the underutilization of labor that currently exists. As the economy strengthens over the next few years, inflation is expected to remain below the Federal Reserve's goal, and interest rates on Treasury securities, which have been exceptionally low since the recession, are projected to rise considerably.

The Budget Deficit Continues to Shrink in 2014, but Federal Debt Is Still Growing

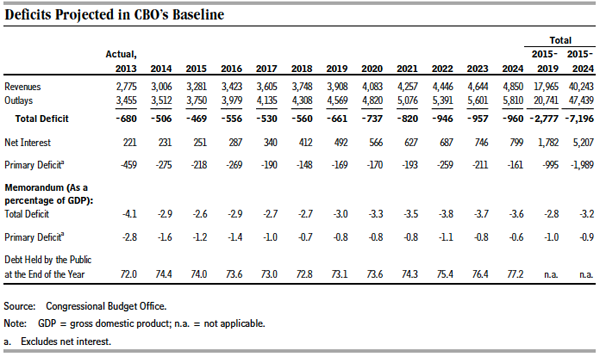

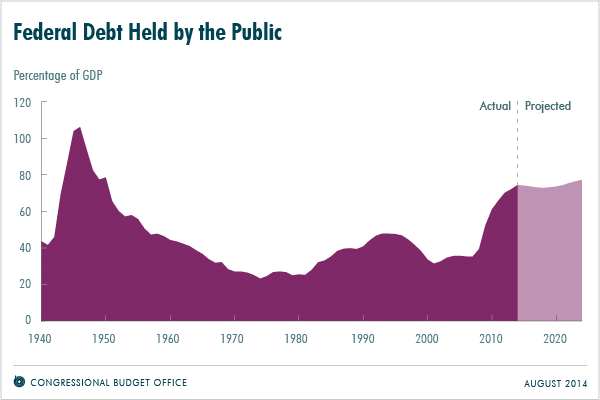

The federal budget deficit for fiscal year 2014 will amount to $506 billion, CBO estimates, roughly $170 billion lower than the shortfall recorded in 2013. At 2.9 percent of gross domestic product (GDP), this year's deficit will be much smaller than those of recent years (which reached almost 10 percent of GDP in 2009) and slightly below the average of federal deficits over the past 40 years. However, by CBO's estimates, federal debt held by the public will reach 74 percent of GDP at the end of this fiscal year—more than twice what it was at the end of 2007 and higher than in any year since 1950.

Outlays

Spending is expected to rise by about 2 percent this year, to $3.5 trillion (see table below). Outlays for mandatory programs, which are governed by statutory criteria and not normally controlled by the annual appropriation process, are projected to rise by about 4 percent. That increase reflects growth in some of the largest programs—including a 15 percent increase in spending for Medicaid and a roughly 5 percent increase in spending for Social Security. In contrast, CBO estimates, net spending for Medicare will increase by only 2 percent in 2014, and spending for some mandatory programs will fall; in particular, outlays for unemployment compensation are expected to drop by nearly 40 percent, primarily because the authority to pay emergency benefits expired at the end of December 2013.

Discretionary spending, which is controlled by annual appropriation acts, is anticipated to be 3 percent less in 2014 than it was in 2013. Nondefense discretionary spending is expected to be about the same this year as it was last year, but defense spending is likely to drop by about 5 percent.

The government's net interest costs will rise by nearly 5 percent this year, CBO estimates, the result of the continued accumulation of debt and higher inflation (which has boosted the cost of the Treasury's inflation-protected securities).

Revenues

Revenues are expected to increase by about 8 percent this year from last year's amounts, to $3.0 trillion. Revenues from all major sources will rise this year, including individual income taxes (by an estimated 6 percent); payroll taxes (by 8 percent); and corporate income taxes (by 15 percent). Increases in wages and salaries and changes in laws—such as those affecting payroll tax rates and income tax deductions for investments in business equipment—largely account for the higher tax receipts. In addition, remittances to the Treasury from the Federal Reserve are anticipated to rise by 33 percent this year, owing to increases in both the size of the Federal Reserve's portfolio of securities and the return on that portfolio.

Persistent Deficits Through 2024 Would Push Debt Relative to GDP Even Higher

CBO regularly produces projections of what federal spending, revenues, and deficits would look like over the next 10 years if current laws governing federal taxes and spending generally remained unchanged. Those baseline projections are designed to serve as a benchmark that policymakers can use when considering possible changes to those laws. According to CBO's updated projections, under current law, the annual deficit would remain less than 3 percent of GDP through 2018, but would grow thereafter, reaching nearly 4 percent from 2022 through 2024. (In contrast, over the past 40 years, deficits averaged 3.1 percent of GDP.)

The persistent and growing deficits that CBO projects would result in increasing amounts of federal debt held by the public. In CBO's baseline projections, that debt rises from 74 percent of GDP this year to 77 percent of GDP in 2024. As recently as 2007, federal debt equaled 35 percent of GDP, but the very large deficits of the past several years caused debt to surge (see figure below).

The large and increasing amount of federal debt would have serious negative consequences, including the following:

- Increasing federal spending for interest payments,

- Restraining economic growth in the long term,

- Giving policymakers less flexibility to respond to unexpected challenges, and

- Eventually increasing the risk of a fiscal crisis (in which investors would demand high interest rates to buy the government's debt).

Outlays

Between 2014 and 2024, annual outlays are projected to grow, on net, by $2.3 trillion, reflecting an average annual increase of 5.2 percent. Boosted by the aging of the population, the expansion of federal subsidies for health insurance, rising health care costs per beneficiary, and mounting interest costs on federal debt, spending for the three fastest-growing components of the budget accounts for 85 percent of the total projected increase in outlays over the next 10 years:

- Annual spending for Social Security is projected to grow by almost 80 percent. Under current law, outlays for that program would climb from 4.9 percent of GDP this year to 5.6 percent in 2024, according to CBO's estimates.

- Annual net outlays for the government's major health care programs (Medicare, Medicaid, the Children's Health Insurance Program, and subsidies for health insurance purchased through exchanges) are projected to rise by more than 85 percent. Outlays for those programs would grow from 4.9 percent of GDP to 5.9 percent, CBO anticipates.

- Outlays for net interest in 2024 are projected to be more than triple those in 2014—the result of both projected growth in federal debt and a rise in interest rates. Net interest outlays would rise from 1.3 percent of GDP this year to 3.0 percent by the end of the coming decade, CBO expects.

In contrast, taken together, all other spending is projected to grow by only about 20 percent. Relative to GDP, such spending would fall—from 9.3 percent this year to 7.3 percent by 2024, its lowest percentage since 1940 (the earliest year for which comparable data have been reported).

Total outlays in the baseline amount to 20.4 percent of GDP in 2014, hover around 21 percent (their average for the past 40 years) from 2015 through 2020, and then rise to about 22 percent from 2022 through 2024. In CBO's projections, both net interest and mandatory spending grow relative to GDP from 2014 to 2024, by 1.7 percent and 1.4 percent, respectively; discretionary spending falls by 1.6 percent of GDP over that period.

Revenues

Revenues are projected to grow by $1.8 trillion between 2014 and 2024, or at an annual rate of 4.9 percent. Provisions of law that have recently taken effect (such as the expiration of certain tax provisions) and, to a lesser extent, the ongoing economic expansion mostly explain a projected jump in federal revenues from this year to next, from 17.5 percent of GDP to 18.3 percent. Greater receipts from individual income taxes (up from 8.1 percent of GDP in 2014 to 8.5 percent in 2015) and corporate income taxes (rising from 1.8 percent of GDP to 2.2 percent) largely account for that increase.

From 2015 through 2024, in CBO's baseline, total revenues change little relative to GDP—amounting to between 18.0 percent and 18.3 percent in each year—because of offsetting factors. Under current law, individual income tax receipts would rise by nearly 1 percent of GDP between 2015 and 2024, reaching 9.4 percent; that increase would occur mainly because a greater proportion of income would fall into higher income tax brackets, a result of tax brackets being indexed for inflation but not for growth in real income. But that rise would be offset both by a decline in corporate income taxes, which are projected to fall to 1.8 percent of GDP in 2024 (mostly because of an expected drop in domestic profits relative to the size of the economy), and by smaller remittances from the Federal Reserve.

Changes From CBO's Previous Budget Projections

The deficit that CBO now estimates for 2014 is a bit larger than the $492 billion the agency projected in April. CBO's estimate of revenues dropped by $26 billion from the April projection, mostly because of lower-than-anticipated receipts from corporate income taxes. CBO's estimate of outlays this year declined by $11 billion, particularly because spending for Medicare and discretionary programs is now expected to be lower than the earlier estimates.

Deficits over the coming decade are now projected to total $7.2 trillion—about $400 billion less than the cumulative deficit CBO projected in April. Although revenues for that period are projected to be lower than the amounts that were previously estimated, projected outlays decline even more, largely because of lower anticipated interest costs.

Economic Growth Will Pick Up in the Next Few Years and Moderate in Later Years

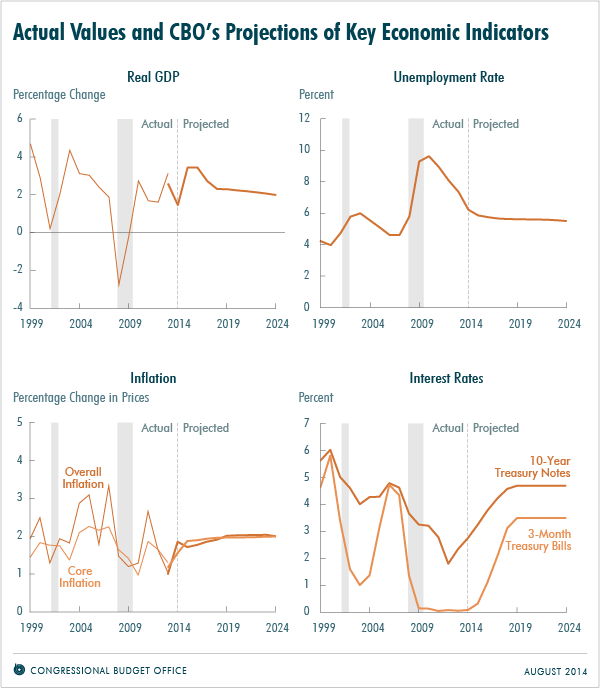

Real (inflation-adjusted) GDP grew at an annual rate of only 0.9 percent during the first half of this calendar year, but CBO expects stronger growth during the second half, in part because the effects of some restraining factors in the first part of the year, such as bad weather, have abated and because recent data, particularly regarding employment, indicate that the economic expansion is on firmer ground. All told, real GDP will increase by 1.5 percent from the fourth quarter of 2013 through the fourth quarter of 2014, CBO estimates.

CBO projects that the growth of real GDP will pick up after this year, to an annual average rate of 3.4 percent from 2014 through 2016 (see figure below). CBO anticipates that growth over the next few years will be stronger than growth this year for three main reasons:

- In response to increased demand for their goods and services, businesses will increase their investments in new structures and equipment at a faster pace and will continue to expand their workforces.

- Consumer spending will also grow more rapidly, spurred by recent gains in household wealth and–with an improving labor market–gains in labor income.

- Fewer vacant housing units, more rapid formation of new households, and further improvement in mortgage markets will lead to larger increases in home building.

The Degree of Slack in the Economy Over the Next Few Years

The faster growth of output will reduce the amount of underutilized productive resources—or “slack”—in the economy over the next few years. CBO estimates that GDP was about 4 percent less than its potential value at the end of last year, but by the end of 2017, that shortfall is expected to narrow to its historical average, which is about ½ percent.

Similarly, the slack in the labor market—reflected in both an elevated unemployment rate and temporary weakness in people's participation in the labor force because of limited job prospects—is expected to largely disappear by the end of 2017. CBO projects that increased hiring will bring the unemployment rate closer to the agency's estimate of the natural rate of unemployment (that is, the rate arising from all sources except fluctuations in the overall demand for goods and services)—reducing it from 6.2 percent in the second quarter of 2014 to 5.6 percent in the fourth quarter of 2017. CBO also expects that the greater hiring will encourage some people to reenter the labor force, slowing both the decline in the unemployment rate and the decline in labor force participation that would result from underlying demographic trends and federal policies by themselves. Nonetheless, CBO anticipates that the labor force participation rate (the percentage of people in the civilian noninstitutionalized population who are age 16 or older and are either working or actively seeking work) will decline slightly—from 62.8 percent in the second quarter of 2014 to 62.3 percent in the fourth quarter of 2017.

Inflation and Interest Rates Over the Next Few Years

Reduced slack in the economy will remove some of the downward pressure on the rate of inflation and interest rates that has existed in the past several years. However, with some slack remaining and with widely held expectations for low inflation, CBO anticipates that the rate of inflation, as measured by the price index for personal consumption expenditures (PCE), will remain below the Federal Reserve's goal of 2 percent during the next few years.

By CBO's estimates, the interest rate on 3-month Treasury bills will remain near zero until the second half of 2015 and then rise to an average of 2.1 percent in 2017; the rate on 10-year Treasury notes is projected to rise from an average of 2.4 percent last year to 4.2 percent in 2017.

The Economic Outlook for 2018 and Later Years

CBO's forecast for 2018 and later years is not based on projections of cyclical developments in the economy, because the agency does not attempt to predict economic fluctuations that far into the future. Instead, the forecast is based on projections of underlying factors that affect the economy's productive capacity.

In CBO's projections, real GDP grows by 2.2 percent per year, on average, between 2018 and 2024—a rate that matches the agency's estimate of the growth of potential output in those years but is notably less than the average growth of potential output during the 1980s and 1990s. That difference largely reflects the retirement of members of the baby boom generation as well as a relatively stable labor force participation rate among working-age women (after decades of strong increases) and the effects of federal tax and spending policies embodied in current law. In addition, the lingering effects of the recent recession and slow recovery are expected to cause the level of GDP to be lower during the 2018–2024 period than it otherwise would be.

Between 2018 and 2024, by CBO's estimates, the un-employment rate will average 5.6 percent (falling slightly over the period, from 5.6 percent to 5.5 percent), and inflation (as measured by the PCE price index) will average 2.0 percent. The interest rate on 3-month Treasury bills will average 3.4 percent during that period, and the rate on 10-year Treasury notes will average 4.7 percent, according to CBO's projections.

Changes From CBO's Previous Economic Projections

CBO's current economic projections differ in some respects from the ones issued in February 2014. The agency has significantly lowered its projection of growth in real GDP for 2014, reflecting surprising economic weakness in the first half of the year. However, the level of real GDP over most of the coming decade is projected to be only modestly lower than estimated in February. In addition, CBO now anticipates lower interest rates throughout the projection period and a lower unemployment rate for the next six years.