At a Glance

The Congressional Budget Office regularly analyzes the distribution of income in the United States and how it has changed over time. This report presents the distributions of household income, means-tested transfers, and federal taxes between 1979 and 2019 (the most recent year for which tax data were available when this analysis was conducted).

- Income. Households at the top of the income distribution received significantly more income than households at the bottom. Between 1979 and 2019, average income, both before and after means-tested transfers and federal taxes, grew for all quintiles (or fifths) of the income distribution, but it increased most among households in the highest quintile.

- Means-Tested Transfers. Means-tested transfers are cash payments and in-kind benefits from federal, state, and local governments that are designed to assist individuals and families who have low income and few assets. Between 1979 and 2019, households in the lowest quintile received more than half of all means-tested transfers. As a percentage of income before transfers and taxes, means-tested transfers rose over the 41-year period, primarily driven by an increase in Medicaid spending.

- Federal Taxes. Higher-income households typically paid a higher average federal tax rate than lower-income households. Average federal tax rates fell between 1979 and 2019 across the income distribution, with the sharpest decline in the lowest quintile.

- Income Inequality. Income inequality, as measured by the Gini coefficients for income both before and after transfers and taxes, rose between 1979 and 2019. (The Gini coefficient is a standard measure of income inequality that summarizes an entire distribution in a single number that ranges from zero to one.) The degree to which transfers and taxes reduced income inequality increased over that same period.

Notes

Numbers in the text, figure, table, and exhibits may not add up to totals because of rounding.

Unless this report indicates otherwise, all years referred to are calendar years.

All dollar amounts are expressed in 2019 dollars and are rounded to the nearest hundred. To convert dollar amounts to 2019 dollars, the Congressional Budget Office used the price index for personal consumption expenditures from the Bureau of Economic Analysis.

Unless this report indicates otherwise, “income” refers to household income before accounting for means-tested transfers and federal taxes, “transfers” refers to means-tested transfers, and “taxes” refers to federal taxes. For additional definitions, see Appendix B.

Specific colors have been used to represent certain income concepts in the exhibits and Figure S-1: Green denotes income before transfers and taxes, blue denotes means-tested transfers, orange denotes federal taxes, and purple denotes income after transfers and taxes.

Supplemental data, additional data for researchers, and a table builder are posted along with this report on CBO’s website (www.cbo.gov/publication/58353#data). The supplemental data and the additional data for researchers present detailed information on income, means-tested transfers, federal taxes, and household types.

Summary

In 2019, household income was unevenly distributed among the roughly 128 million households in the United States, which received a total of about $15.4 trillion in annual income, the Congressional Budget Office estimates.1 The agency estimates that the average income among households in the highest quintile (or fifth) of the income distribution was 14 times the average income of households in the lowest quintile:

- Average income before means-tested transfers and federal taxes among households in the lowest quintile of the income distribution was about $23,800.

- Average income before transfers and taxes among households in the highest quintile was about $332,100.

Furthermore, income within the highest quintile was skewed toward the very top of the distribution: Average income before transfers and taxes among households in the bottom half of the highest quintile (the 81st to 90th percentiles) was about $180,100; average income among the 1.2 million households in the top 1 percent of the distribution was about $2.0 million; and average income among the approximately 12,000 households in the top 0.01 percent of the distribution was about $43.0 million.2

Income before transfers and taxes consists of market income and social insurance benefits (such as benefits from Social Security and Medicare) and excludes means-tested transfers and federal taxes.3 Means-tested transfers are cash payments and in-kind benefits from federal, state, and local governments that are designed to assist individuals and families who have low income and few assets. They include benefits from government programs such as Medicaid and the Children’s Health Insurance Program (CHIP), the Supplemental Nutrition Assistance Program (SNAP, formerly known as the Food Stamp program), and Supplemental Security Income (SSI). Federal taxes consist of individual income taxes (net of refundable tax credits, such as the earned income tax credit and the child tax credit), payroll taxes, corporate income taxes, and excise taxes.

For this report, CBO focused on the distribution of household income in 2019, the most recent year for which relevant data from tax returns were available.4 In addition, CBO assessed trends in household income, means-tested transfers, federal taxes, and income inequality over the 41-year period beginning in 1979 and ending in 2019.5

Many households experience changes in their income, transfers, taxes, or household composition from year to year. As a result, the households in any given group of the income distribution in 2019 do not represent the same households that were in that group in prior years.6 Therefore, this analysis focuses on the changes in the overall distribution of household income rather than the experiences of particular households.

How Did Means-Tested Transfers and Federal Taxes Affect Household Income in 2019?

Federal fiscal policies have significant effects on the economic resources available to U.S. households.7 Before means-tested transfers and federal taxes are taken into account, average income among all households in 2019 was $119,600, CBO estimates. Means-tested transfers provided households with an additional $5,900 in income, on average, in that year. Federal taxes amounted to $23,200 per household, on average. The net effect of means-tested transfers and federal taxes was to decrease household income by $17,300, on average, bringing average household income after transfers and taxes to $102,400 in 2019.

Those averages, however, obscure a significant amount of variation in household income and in how means-tested transfers and federal taxes affect income. In 2019, means-tested transfers and federal taxes caused household income to be more evenly distributed (see Figure S-1, upper panel). On average, households in the lower quintiles received more in transfers than they paid in taxes, while households at the higher end of the income distribution paid more in taxes than they received in transfers. Those transfers and taxes had the following effects:

- They increased income among households in the lowest quintile by $15,100 (or 64 percent), on average, to $38,900; and

- They decreased income among households in the highest quintile by $80,000 (or 24 percent), on average, to $252,100.

Furthermore, within that highest quintile, income after transfers and taxes was significantly higher among households at the top of the distribution. Among households in the 81st to 90th percentiles, transfers and taxes reduced income by $34,800, on average, to $145,300. They decreased income by about $600,000, on average, in the top 1 percent of the distribution, to $1.4 million. Among households in the top 0.01 percent of the distribution, they reduced income by $13.0 million, on average, to $30.0 million. Although transfers and taxes reduce income inequality, income after transfers and taxes remains skewed toward the top of the income distribution.

Figure S-1.

Average Income, Means-Tested Transfers, and Federal Taxes, 2019, and Cumulative Growth in Average Income, 1979 to 2019

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of a recession. (A recession extends from the peak of a business cycle to its trough.)

All dollar amounts are expressed in 2019 dollars.

To calculate growth rates, CBO first converted all dollar amounts to 2019 dollars using the Bureau of Economic Analysis’s price index for personal consumption expenditures.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

* = between zero and $500.

How Were Means-Tested Transfers and Federal Taxes Distributed in 2019?

In 2019, the average means-tested transfer rate among all households was about 5 percent, CBO estimates—that is, in total, means-tested transfers received by households were equal to 5 percent of all income before transfers and taxes. However, the average rate varied significantly by income group. Among households in the lowest quintile of the income distribution (ranked by income before transfers and taxes), the average means-tested transfer rate was about 64 percent; among households in the middle quintile, the average rate was about 4 percent; and among households in the highest quintile, the average rate was less than one-half of one percent.

In 2019, the average federal tax rate (based on tax liabilities incurred during that calendar year) also varied significantly by income group. Among all households it was about 19 percent, CBO estimates. Among households in the lowest quintile, the average rate was 0.5 percent, on net; in the middle quintile it was about 13 percent; and in the highest quintile it was about 24 percent. The average federal tax rate among households in the top 1 percent of the income distribution in 2019 was about 30 percent.

Thus, both means-tested transfers and federal taxes are progressive—that is, low-income households receive a larger share of their income as means-tested transfers than high-income households do, and high-income households pay a larger share of their income in federal taxes than low-income households do. In 2019, means-tested transfers went overwhelmingly to low-income households—just over half of such transfers went to households in the lowest income quintile, and nearly a quarter went to households in the second quintile.

Not all households receive means-tested transfers, but virtually all households pay federal taxes in some form (individual income taxes, payroll taxes, corporate taxes, or excise taxes). However, some households near the lower end of the income distribution have net negative average federal tax rates—that is, refundable tax credits exceed the payroll taxes, corporate taxes, and excise taxes paid by those households.

Households at the top of the income distribution pay the majority of federal taxes. Households in the highest income quintile, which received about 55 percent of all income, paid more than two-thirds of all federal taxes in 2019, CBO estimates. In contrast, households in the lowest quintile, which received about 4 percent of all income, paid about 0.1 percent of federal taxes, on net, in that year.

Because of the progressive structure of means-tested transfers and federal taxes, the distribution of income after transfers and taxes was more even than the distribution of income before transfers and taxes. In 2019, those transfers and taxes boosted the lowest quintile’s share of total income by nearly 4 percentage points, CBO estimates. In contrast, among households in the highest quintile, the share of income after transfers and taxes was roughly 6 percentage points lower than the share of income before transfers and taxes.

What Are the Trends in Household Income and Income Inequality?

According to CBO’s estimates, between 1979 and 2019, average household income before transfers and taxes grew more among households at the top of the income distribution than among those at the bottom. Among households in the highest quintile, average real income (that is, income adjusted to remove the effects of inflation) in 2019 was 114 percent higher than it was in 1979. In contrast, among households in the lowest quintile, average income before transfers and taxes was 45 percent greater in 2019 than in 1979, and among households in the middle three quintiles, it was 43 percent greater in 2019 than in 1979 (see Figure S-1, lower panel). Because of those differences in cumulative growth rates, income inequality was greater in 2019 than it was in 1979.

From 1979 to 2019, among households in the lowest income quintile, cumulative growth in income after transfers and taxes was greater than cumulative growth in income before transfers and taxes—94 percent versus 45 percent. That faster growth is attributable both to an increase in spending on Medicaid and CHIP and to a reduction in federal taxes—the latter largely the result of increased refundable tax credits provided through the individual income tax.

Among households in the middle three income quintiles (the 21st to 80th percentiles), the expansion of means-tested transfers and generally declining average federal tax rates had a similar effect. Specifically, cumulative growth in income after transfers and taxes was larger for those groups than it was before transfers and taxes—59 percent versus 43 percent.

In the highest quintile, cumulative growth in income after transfers and taxes was also greater than growth in income before transfers and taxes—123 percent versus 114 percent. Households in the top 1 percent of the income distribution experienced the largest cumulative growth in income after transfers and taxes. In 2019, real income after transfers and taxes for that income group was 262 percent greater than it was in 1979, CBO estimates.

Overall, transfer programs and the tax system reduced income inequality by more in 2019 than they did in 1979. Consequently, inequality of income after transfers and taxes increased by less than inequality of income before transfers and taxes.

What Is New in This Report?

This report incorporates new tax data for 2019—the year preceding the onset of the coronavirus pandemic. Because those data are based on tax returns filed in 2020, they may have been affected by the pandemic and by subsequent delays to tax-filing deadlines.

The report does not show the effects of federal programs, such as economic impact payments and expanded unemployment payments, that were enacted in response to the pandemic. Those programs will be addressed in The Distribution of Household Income, 2020, which CBO will publish once the relevant tax data are available.

In 2019, income growth was strong across the five quintiles, with each quintile reaching record levels of income before transfers and taxes. Income gains were larger for lower-income households than for higher-income households: Specifically, the lowest quintile’s income grew by 7 percent between 2018 and 2019. By contrast, income in the middle quintile grew by 4 percent and, in the top quintile, by 1 percent. Among households in the top 1 percent of the income distribution, however, income before transfers and taxes declined for the second straight year, remaining below its 2007 peak.

As a result of strong income growth, means-tested transfer rates declined in the lowest quintiles, which receive most of such transfer income. Average tax rates, which continued to reflect the effects of Public Law 115-97 (referred to as the 2017 tax act throughout this report), rose among the bottom three quintiles by 0.3 percentage points to 0.7 percentage points. Those increases were driven by increases in individual income tax rates, reflecting higher levels of income. Meanwhile, tax rates were constant in the top two quintiles.

Higher average tax rates and lower transfer rates tempered some of the growth in income for the bottom two quintiles. Growth in income after transfers and taxes ranged from 3 percent to 4 percent for each of the bottom four quintiles, whereas the top quintile’s income after transfers and taxes grew by 2 percent.

Income Before Transfers and Taxes

Income before transfers and taxes consists of market income plus social insurance benefits. Market income comprises wages and other forms of labor income (including cash wages, employers’ contributions for health insurance premiums, and payroll taxes paid by employers), business income, capital income (including capital gains), and other income sources. Social insurance benefits include Social Security and Medicare benefits, unemployment insurance, and workers’ compensation. Notably, income before transfers and taxes excludes the effects of government policies carried out through means-tested transfer programs or the federal tax system.

Income before transfers and taxes is skewed toward households at the top of the income distribution. As a result, those households receive a substantial share of income before transfers and taxes.

The composition of income before transfers and taxes varies throughout the distribution. For most households, labor income is the majority of income before transfers and taxes. But among households at the top of the income distribution, capital income constitutes a greater portion of income before transfers and taxes than it does for the rest of households. Additionally, as income rises, social insurance benefits tend to decline as a share of income.

Between 1979 and 2019, income before transfers and taxes grew faster in real terms among households in the highest quintile of the distribution than among households in the lower quintiles. As a result, the share of income before transfers and taxes received by the highest income quintile increased over that 41-year period.

Exhibit 1.

Average Household Income Before Transfers and Taxes, 2019

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

All dollar amounts are expressed in 2019 dollars.

Income groups are created by ranking households by income before transfers and taxes, adjusted for household size. Each quintile (fifth) contains approximately the same number of people. The lowest quintile does not include households with negative income, which are less than one-half of one percent of households.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Income before transfers and taxes was skewed toward the top of the income distribution in 2019. Among households in the highest quintile, average income before transfers and taxes was $332,100 that year, compared with $81,800 among households in the middle quintile and $23,800 among those in the lowest quintile.

Moreover, income before transfers and taxes was skewed toward the very top of the distribution within the highest quintile. Average income before transfers and taxes among households in the 81st to 90th percentiles (the lower half of the highest quintile) was $180,100 in 2019, whereas income among households in the top 1 percent of the distribution (1.2 million households) averaged $2.0 million.

Income within the top 1 percent also varied widely: Average income before transfers and taxes among households in the top 0.01 percent was $43.0 million in 2019, compared with $5.7 million among households in the 99.9th to 99.99th percentiles and $1.2 million among those in the 99th to 99.9th percentiles.

Exhibit 2.

Composition of Income Before Transfers and Taxes, 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Other market income includes income received in retirement for past services and other nongovernmental sources of income.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

* = between zero and 0.5 percent.

The composition of income before transfers and taxes varied throughout the distribution in 2019. Labor income constituted the majority of income for most income groups, except the top 1 percent.

Among households in the lowest quintile and in the top 1 percent of the distribution, labor income accounted for a smaller proportion of average income before transfers and taxes than among those in between. In the lowest quintile, labor income was 61 percent of income before transfers and taxes in 2019, compared with 69 percent among households in the middle three quintiles and in the 81st to 99th percentiles. Within the top 1 percent, labor income was, on average, just one-third of income before transfers and taxes in 2019.

Among the top 1 percent of the distribution, business income and capital income (including capital gains) were, on average, a larger percentage of income than in lower income groups. Among households in the top 0.01 percent, capital income (including capital gains) accounted for an average of 70 percent of income before transfers and taxes in 2019.

On average, social insurance benefits were a greater portion of income before transfers and taxes among households in the lowest quintile than among higher-income households. Social insurance benefits were more than one-quarter of income before transfers and taxes among households in the lowest quintile, compared with 4 percent among households in the highest quintile.

Exhibit 3.

Trends in the Distribution of Income Before Transfers and Taxes, 1979 to 2019

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

All dollar amounts are expressed in 2019 dollars.

To calculate growth rates, CBO first converted all dollar amounts to 2019 dollars using the Bureau of Economic Analysis’s price index for personal consumption expenditures.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Average income before transfers and taxes grew in real terms between 1979 and 2019 among households in each quintile. That growth was unevenly distributed. Among households in the highest quintile, average income before transfers and taxes increased by 114 percent over the 41-year period (or at an average annual rate of 1.9 percent), from $154,900 in 1979 to $332,100 in 2019 (in 2019 dollars). By comparison, average income before transfers and taxes grew by a cumulative 45 percent among households in the lowest quintile (from $16,300 in 1979 to $23,800 in 2019, or at an average annual rate of 0.9 percent) and by 43 percent among those in the middle three quintiles (from $60,000 in 1979 to $85,700 in 2019, or at an average annual rate of 0.9 percent).

Compared with the rest of the distribution, households in the highest quintile received a larger share of their income as capital income, which tends to rise or fall more with the economy than other forms of income. As a result, that quintile experienced the largest relative swings in income before transfers and taxes over economic cycles. For example, during the 2007–2009 recession, the highest quintile’s average income before transfers and taxes fell by 18 percent, compared with 5 percent among households in the middle three quintiles and 4 percent among those in the lowest quintile.

In 2019, average income before transfers and taxes in each of the five quintiles reached its highest level over the entire 41-year period. Compared with average income in 2018, average income among households in the lowest quintile increased by 7 percent in 2019, the highest annual growth rate since 1995.

Exhibit 4.

Cumulative Growth in Income Before Transfers and Taxes Among Households in the Highest Quintile, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

To calculate growth rates, CBO first converted all dollar amounts to 2019 dollars using the Bureau of Economic Analysis’s price index for personal consumption expenditures.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Average income before transfers and taxes more than doubled for households in the highest quintile between 1979 and 2019. It grew faster among households at the very top of the income distribution than among others in that quintile. Over the 41-year period, income before transfers and taxes grew by the following amounts:

- 89 percent among households in the 81st to 99th percentiles, or at an average annual rate of 1.6 percent, from $131,000 to $247,300;

- 178 percent among households in the 99th to 99.9th percentiles, or at an average annual rate of 2.6 percent, from $423,400 to $1.2 million;

- 321 percent among households in the 99.9th to 99.99th percentiles, or at an average annual rate of 3.7 percent, from $1.4 million to $5.7 million; and

- 424 percent among households in the top 0.01 percent of the distribution, or at an average annual rate of 4.2 percent, from $8.2 million to $43.0 million.

Income volatility tends to be greater among higher income groups because households in such groups derive a large portion of their income from capital income, which fluctuates more in response to economic conditions than labor income does. Those fluctuations affect the income of individual households, contributing to the year-to-year changes in the set of households included in higher income groups.

Exhibit 5.

Composition of Income Before Transfers and Taxes Among Households in the Top 1 Percent, 1979 to 2019

Millions of Dollars

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

All dollar amounts are expressed in 2019 dollars.

Other market income includes income received in retirement for past services and other nongovernmental sources of income.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

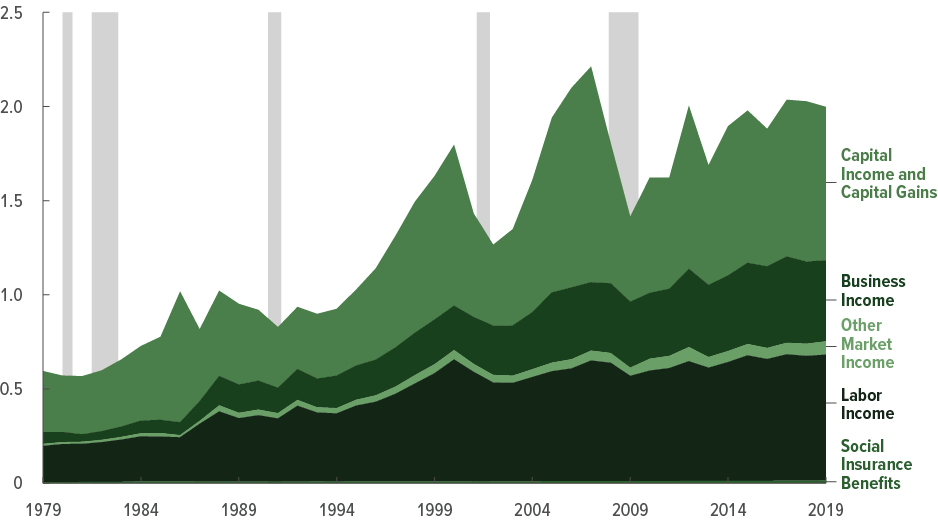

Between 1979 and 2019, the composition of income before transfers and taxes changed among households in the top 1 percent of the distribution, as different forms of income grew at different rates. (Additionally, changes in tax laws affected how certain forms of income were categorized over the period.)

Of the five components of income before transfers and taxes, business income expanded fastest, growing nearly sevenfold over the 41-year period. As a share of income among households in the top 1 percent, business income rose from 11 percent in 1979 to 22 percent in 2019. Meanwhile, average capital income (including capital gains) grew at a slower pace than other forms of income. As a result, it declined as a share of income among households in the top 1 percent of the distribution, from 54 percent in 1979 to 41 percent in 2019. Labor income remained roughly constant at about one-third of income among such households from 1979 to 2019. Within that income group, other market income and social insurance benefits together made up, on average, less than 4 percent of income during the period.

Between 1979 and 2019, capital income was more volatile than other forms of income. Much of that volatility was attributable either to year-to-year changes in asset prices (the largest changes within that period occurred in 2001 and 2007) or to behavioral responses to changes in tax laws (for example, in 1986 and 2012).

Exhibit 6.

Shares of Income Before Transfers and Taxes, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shares do not add up to 100 percent because households with negative income are not shown.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Between 1979 and 2019, the highest quintile’s share of income before transfers and taxes increased. In total, that group received more than half of all income before transfers and taxes in 2019, whereas the lowest quintile received 4 percent. The share of income before transfers and taxes among households in the top 1 percent of the distribution was 16 percent in 2019, CBO estimates.

Between 1979 and 2019, the share of income among the top 1 percent increased by 7 percentage points. Meanwhile, the share of income among the middle three quintiles fell by 7 percentage points, and the lowest quintile’s share fell by 1 percentage point.

The share of income before transfers and taxes among the top 1 percent of the distribution tended to increase during economic expansions and fall during economic downturns. That group’s share of income in 2019 remained below its 2007 peak of 19 percent.

Means-Tested Transfers

Means-tested transfers are cash payments and in-kind benefits from federal, state, and local governments that are designed to assist individuals and families who have low income and few assets. This analysis focuses on the average means-tested transfer rate, which is the ratio of average means-tested transfers to average income before transfers and taxes in a given income group.

Means-tested transfers go largely to households near the bottom of the income distribution.8 In 2019, more than half of means-tested transfers went to households in the lowest quintile.9 Between 1979 and 2019, means-tested transfer rates doubled among households in that quintile—growth that is attributable both to increases in the number of people receiving benefits and increases in the average cost of those benefits per recipient.

Eligibility for some means-tested transfer programs has expanded since 1979. Consequently, means-tested transfers provided to individuals and families in the second and the middle income quintiles increased over the 1979–2019 period.

Over that 41-year period, growth in means-tested transfer rates was primarily driven by spending on Medicaid, which was the largest—and fastest growing—means-tested transfer program. During that time, the number of people enrolled in Medicaid or CHIP increased almost fivefold, from about 20 million in 1979 to 95 million in 2019.10 Furthermore, the average benefit per recipient (in 2019 dollars) increased from $1,800 in 1979 to $5,900 in 2019.11 Meanwhile, total spending on SNAP, SSI, and other transfers was roughly constant as a share of income between 1979 and 2019.

Exhibit 7.

Average Means-Tested Transfer Rates Among Selected Income Groups, by Type of Transfer, 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Average means-tested transfer rates for both the fourth quintile and the highest quintile are less than 0.5 percent for all sources and transfer programs, except the average transfer rate for Medicaid in the fourth quintile, which is 1.3 percent.

Other transfers consist of housing assistance programs; low-income subsidies for Part D of Medicare (which covers prescription drugs); Temporary Assistance for Needy Families; child nutrition programs; cost-sharing reductions under the Affordable Care Act; the Low Income Home Energy Assistance Program; and state and local government general assistance programs.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

CHIP = Children’s Health Insurance Program; SNAP = Supplemental Nutrition Assistance Program; SSI = Supplemental Security Income; * = between zero and 0.5 percent.

In 2019, average means-tested transfer rates were highest among households in the lowest quintile, at 64 percent—that is, in total, means-tested transfers received by households in that quintile equaled 64 percent of all income before transfers and taxes in the quintile. For each of the four categories of means-tested transfer programs, average transfer rates were highest in the lowest quintile and declined as income rose.

Medicaid and CHIP make up 73 percent of all means-tested transfers analyzed in this report (as measured by the average cost to the government of providing those benefits). Among households in the lowest quintile, average Medicaid and CHIP benefits were 44 percent of average income before transfers and taxes. Medicaid and CHIP transfer rates were 11 percent in the second quintile and 4 percent in the middle quintile.

SNAP constitutes about 7 percent of all means-tested transfers analyzed here. The average SNAP transfer rate in the lowest quintile was 6 percent. It was less than 1 percent in the second and middle quintiles.

SSI accounts for about 7 percent of means-tested transfers. Among households in the lowest quintile, the average SSI transfer rate was 5 percent, compared with less than 1 percent in the second and middle quintiles.

Together, programs categorized as “Other Transfers” make up about 12 percent of means-tested transfers. Among households in the lowest quintile, the average rate for other transfers was 9 percent.

Exhibit 8.

Average Means-Tested Transfer Rates Among Selected Income Groups, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

Average means-tested transfer rates for the highest two quintiles have been less than 2 percent since 1979.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Beginning in the early 1980s, means-tested transfers as a share of total income increased among households in the bottom three quintiles. The average means-tested transfer rate doubled among households in the lowest income quintile, rising from 32 percent in 1979 to 64 percent in 2019. Over that period, it also increased from 2 percent to 14 percent among households in the second quintile and from 1 percent to 4 percent among households in the middle quintile.

Expansions in eligibility and increased government spending on transfer programs contributed to rising means-tested transfer rates over the 41-year period. Increases in Medicaid enrollment and costs accounted for more than 80 percent of the growth in means-tested transfer rates in every quintile between 1979 and 2019. Within the lowest quintile, the average means-tested transfer rate peaked at 75 percent in 2014 after many states expanded Medicaid eligibility under the Affordable Care Act, but it began to decline afterward as income grew faster than transfers, on average.

Over the 41-year period, means-tested transfer rates generally rose during recessions, particularly among households in the lowest quintile, as income decreased and more households became eligible for transfers. That growth typically continued for several years after each recession before declining during periods of economic expansion. From 2018 to 2019, average income before transfers and taxes grew by 7 percent among households in the lowest quintile, whereas average transfers fell by 1 percent, contributing to a 6 percentage-point decrease in that quintile’s means-tested transfer rate.

Exhibit 9.

Average Means-Tested Transfer Rates Among Households in the Lowest Quintile, by Type of Transfer, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

Other transfers consist of housing assistance programs; low-income subsidies for Part D of Medicare (which covers prescription drugs); Temporary Assistance for Needy Families; child nutrition programs; cost-sharing reductions as part of the Affordable Care Act; the Low Income Home Energy Assistance Program; and state and local government general assistance programs.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

CHIP = Children’s Health Insurance Program; SNAP = Supplemental Nutrition Assistance Program; SSI = Supplemental Security Income.

Between 1979 and 2019, the growth of means-tested transfers as a percentage of income for low-income households varied by program. Medicaid (along with CHIP) was the fastest-growing means-tested transfer program over the period. Among households in the lowest quintile, the average rate of Medicaid and CHIP transfers increased from 9 percent in 1979 to 44 percent in 2019. That growth is attributable to increases in the number of households receiving benefits and in the average cost of those benefits per recipient. Transfer rates rose after legislative expansions—after CHIP was introduced in 1998, for example, and after major provisions of the Affordable Care Act were implemented in 2014.

Transfer rates for SNAP, SSI, and other benefit programs changed less than those for Medicaid and CHIP over the same period. Among households in the lowest quintile, the SNAP rate was 6 percent in 1979 and in 2019, and the SSI rate was 5 percent in both years. The rate for other transfers fell from 12 percent to 9 percent.

Transfer rates for each program grew during economic recessions, but the extent of the growth varied. During the 2007–2009 recession, Medicaid, CHIP, and SNAP rates increased for the lowest quintile, in part because more people became eligible for those programs. Rates for SSI and other transfers also increased for that quintile, but by less. In 2019, average transfer rates for each program fell as the lowest quintile’s average income before transfers and taxes increased.

Federal Taxes

In this analysis, federal taxes consist of individual income taxes, payroll taxes, corporate income taxes, and excise taxes. The taxes allocated to households in the analysis account for approximately 93 percent of all federal revenues collected in 2019.12 Individual income taxes and payroll taxes are the largest sources of tax revenues, followed by corporate taxes and excise taxes.13 CBO’s examination of household income focuses on the average federal tax rate, which is calculated by dividing total federal taxes in an income group by total income before transfers and taxes in that group.14

Average federal tax rates generally rise with income. Households in the highest income quintile, which received about 55 percent of all income in 2019, paid more than two-thirds of federal taxes that year. In contrast, households in the lowest quintile, which received about 4 percent of all income, paid about 0.1 percent of federal taxes, on net, that year. Among households in the lowest two quintiles, individual income taxes are negative, on average, because they include refundable tax credits, which can result in net payments from the government.15

Year-to-year fluctuations in average federal tax rates are caused both by underlying changes in the income distribution and by legislative changes to federal tax rules.16 For most income groups, the average federal tax rate fell over the 41-year period analyzed here; the lowest income quintile experienced the sharpest decrease. The average federal tax rate among households in the middle of the income distribution also decreased but not as much as it did among households in the lowest quintile. In contrast, the average federal tax rate for households in the 81st to 99th percentiles of the income distribution was relatively stable over the 1979–2019 period. The average rate for the top 1 percent of the distribution was significantly more volatile than the average rate for other income groups.

Exhibit 10.

Average Federal Tax Rates, by Income Group, 2019

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Income groups are created by ranking households by income before transfers and taxes, adjusted for household size. Each quintile (fifth) contains approximately the same number of people. The lowest quintile does not include households with negative income, which are less than one-half of one percent of households.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Average federal tax rates generally rise with income. In 2019, average federal tax rates were higher among higher income groups than among lower income groups. The highest quintile’s average federal tax rate was 24 percent, compared with 13 percent for the middle quintile. The lowest quintile’s average federal tax rate was 0.5 percent, on net, because refundable credits offset the taxes paid by that group (see Exhibit 13). Within the highest quintile, average tax rates were higher at the top of the distribution, averaging 30 percent among households in the top 1 percent.

Within that top 1 percent, average tax rates were relatively flat. Households in the highest income group face higher average corporate tax rates, but lower individual income tax rates. That group receives a larger share of its income as capital income, which is generally taxed at a lower rate than other forms of individual income. (For example, in 2019, the top long-term capital gains tax rate was 20 percent, whereas the top marginal individual income tax rate was 37 percent.)

Exhibit 11.

Average Federal Tax Rates, by Income Group, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Between 1979 and 2019, the average federal tax rate declined most sharply among households in the lowest quintile, falling from a peak of 12.1 percent in 1984 to 0.5 percent, on net, in 2019. The introduction and expansion of refundable tax credits lowered the average individual tax rate among low-income taxpayers, particularly between 2007 and 2009, and in 2018 (see Exhibit 15). Average federal tax rates also declined among the middle three quintiles (from 19.3 percent in 1979 to 13.9 percent in 2019) and among the 81st to 99th percentiles (from 25.1 percent in 1979 to 22.1 percent in 2019).

Among households in the top 1 percent of the income distribution, the average federal tax rate began to fall in the late 1990s and then rose in 2013. That dip coincided with reductions in the top statutory marginal individual income tax rate and the tax rate on dividends and capital gains in the late 1990s and early 2000s. In 2013, the top marginal tax rate returned to 39.6 percent, just as higher tax rates on capital gains and new taxes enacted as part of the Affordable Care Act went into effect.

In 2018, the average federal tax rate for each income group fell, following the enactment of the 2017 tax act, which made numerous changes, including reducing statutory marginal tax rates. The average federal tax rate rose for the lower three quintiles in 2019, reflecting brisk income growth.

Exhibit 12.

Average Federal Tax Rates Among Households in the Top 1 Percent, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

The average federal tax rate among households in the top 1 percent of the income distribution has varied over time, ranging from a high of 35 percent in 1979 to a low of 25 percent in 1986. Average federal tax rates generally moved in tandem across the three subgroups of the top 1 percent; however, the rates diverged in the early 1980s, mid-1990s, and mid-2010s.

During the mid-1990s and mid-2010s, the average federal tax rate among households in the top one-tenth of one percent of the distribution (that is, the top 0.01 percent and the 99.9th to 99.99th percentiles combined) increased more than that of the 99th to 99.9th percentiles in response to changes in tax laws. In 1993 and 2013, the top marginal individual income tax rate increased to 39.6 percent. Because higher-income households had more income subject to the top rate, the top 0.1 percent’s average federal tax rate increased more than that of the 99th to 99.9th percentiles.

In general, households in higher income groups tended to pay higher average federal tax rates than households in lower income groups. However, in most years following the late 1990s, households in the top 0.01 percent paid a lower average federal tax rate than did households in the 99.9th to 99.99th percentiles because a larger portion of the former group’s income consisted of capital income, which is generally taxed at lower rates under the individual income tax. That group’s average federal tax rate tended to fall in periods with large capital gains, such as the late 1990s, the mid-2000s, and 2017.

Exhibit 13.

Average Federal Tax Rates, by Tax Source, 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

* = between zero and 0.5 percent.

Of the four types of federal taxes included in this analysis, the individual income tax is the most progressive. Average individual income tax rates in 2019 ranged from –11 percent in the lowest quintile to 15 percent in the highest quintile. For the two lowest quintiles, average individual income tax rates were negative because of refundable tax credits (see Exhibit 15).

Average payroll tax rates were lower at the top of the income distribution because a greater share of those households’ earnings was above the maximum amount subject to Social Security payroll taxes ($132,900 in 2019), which is also the maximum amount included in the computation of benefits. Average payroll tax rates for the lower four quintiles were about 9 percent, but the average was 6.5 percent among households in the highest quintile.

The average corporate income tax borne by households increases with income. In 2019, the average corporate tax rate was 2.2 percent among households in the highest quintile and 4.2 percent among households in the top 1 percent of the distribution.

Excise taxes are regressive: The amount of excise taxes paid relative to income is greatest for lower-income households, which tend to spend a larger share of their income on taxed goods and services. In 2019, the average excise tax rate was 1.7 percent for the lowest quintile, compared with 0.8 percent for the middle quintile and 0.4 percent for the highest quintile.

Exhibit 14.

Average Federal Tax Rates, by Tax Source, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

In 2019, the average federal tax rate among all households in the United States was 19 percent, which was less than the average rate for the entire 1979–2019 period (21 percent). Each of the four federal taxes that combine to make up that average—individual income taxes, payroll taxes, corporate income taxes, and excise taxes—had a distinct pattern over the 41-year period.

Over that period, the average individual income tax rate ranged from a high of 12.1 percent in 1981 to a low of 7.5 percent in 2009. In 2019, the average individual income tax rate was 9.3 percent, a decline of 1.2 percentage points from 2017. Provisions included in the 2017 tax act contributed to that decrease (see the section titled “The Distributional Effects of the 2017 Tax Act in 2018” in the 2018 edition of this report).

In 2019, the average payroll tax rate was 7.8 percent, having held roughly constant since 2015. That rate was just below the 41-year average payroll tax rate of 7.9 percent. Payroll taxes fell in 2011 and 2012 because of a reduction in the Social Security payroll tax rate but rose again in 2013, when the Medicare payroll tax rate was increased for high-income taxpayers.

The average corporate tax rate among all households fell from 3.4 percent in 1979 to 1.5 percent in 2019. From 2014 through 2019, it declined each year. The average excise tax rate, the smallest component of the overall federal tax rate, was relatively stable over the entire 1979–2019 period, amounting to 1.0 percent in 1979 and 0.6 percent in 2019.

Exhibit 15.

Average Refundable Tax Credit Rates Among Selected Income Groups, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

Major individual income tax credits consist of the earned income tax credit; the child tax credit; postsecondary education tax credits (the American Opportunity Tax Credit—formerly the Hope credit—and the Lifetime Learning credit); the premium tax credit; the 2008 economic stimulus payments; and the Making Work Pay tax credit. Major individual income tax credits include both the refundable and nonrefundable portions of the credit, when applicable.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

In 1979, the earned income tax credit (EITC) was the only refundable tax credit in effect. Since then, several additional refundable tax credits have been enacted, including the child tax credit in 1998 and the premium tax credit for health insurance coverage established by the Affordable Care Act in 2014. Additionally, lawmakers increased the credit amount and income parameters of the EITC and the child tax credit several times over the years, including an expansion of the child tax credit in the 2017 tax act that took effect in 2018. As a result, among households in the lowest income quintile, the refundable tax credit rate—that is, total refundable tax credits divided by total income before transfers and taxes—increased from 1.2 percent in 1979 to 12.4 percent in 2019.

Because of refundable tax credits, the average individual income tax rates among households in the lowest and second quintiles were negative in 2019: –11 percent and –2 percent, respectively (see Exhibit 13). Without those tax credits, the average individual income tax rate for those two quintiles would have been positive: about 1 percent and 3 percent, respectively.

Each refundable credit has its own eligibility criteria and therefore varies in its response to economic changes. The two largest credits, the EITC and the child tax credit, tend to increase during economic recessions. Also, two temporary refundable credits were enacted during the 2007–2009 recession. Overall, the average refundable tax credit rate for the lowest quintile rose by 6 percentage points between 2007 and 2009, reaching 14.2 percent, its highest level over the 41-year period.

Exhibit 16.

Shares of Federal Taxes, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shares do not add up to 100 percent because households with negative income are not shown.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

The share of federal taxes paid by households in the highest quintile increased from 55 percent in 1979 to 69 percent in 2019. That group’s share of income before transfers and taxes also increased over the period but by less than its share of federal taxes. Most of that 14 percentage-point increase in the federal tax share occurred in the top 1 percent of the income distribution, whose share of all federal taxes rose by 11 percentage points, from 14 percent in 1979 to 25 percent in 2019. Those households’ share of income before transfers and taxes also rose, although to a lesser extent: from 9 percent in 1979 to 16 percent in 2019.

Between 1979 and 2019, the shares of individual income taxes, payroll taxes, and corporate taxes became increasingly concentrated in the highest quintile, whereas the distribution of shares of excise taxes remained relatively constant. The highest quintile’s share of individual income taxes rose from 65 percent in 1979 to 90 percent in 2019; its share of payroll taxes rose by 9 percentage points; and its share of corporate taxes rose by 10 percentage points.

Over the 41-year period, the share of taxes paid by higher-income households exceeded their share of income; the opposite was true for lower-income households. In 2019, households in the highest quintile received 55 percent of income before transfers and taxes and paid 69 percent of federal taxes. Households in the lowest quintile received 4 percent of income before transfers and taxes and paid about 0.1 percent of federal taxes, on net.

Income After Transfers and Taxes

Income after transfers and taxes is income before transfers and taxes plus means-tested transfers minus federal taxes. Because of the progressivity of means-tested transfers and federal taxes (driven primarily by the size and structure of the individual income tax), income after transfers and taxes is less skewed toward households at the top of the distribution than income before transfers and taxes. From 1979 to 2019, income after transfers and taxes grew more evenly across the income distribution than income before transfers and taxes.

The average income after transfers and taxes of households in different income groups grew at different rates because of changes in means-tested transfer programs, federal tax laws, and economic conditions. Income grew significantly faster among households in the highest quintile than among all other income groups, mainly because of changes in income before transfers and taxes.

Exhibit 17.

Average Household Income After Transfers and Taxes, 2019

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

All dollar amounts are expressed in 2019 dollars.

Income groups are created by ranking households by income before transfers and taxes, adjusted for household size. Each quintile (fifth) contains approximately the same number of people. The lowest quintile does not include households with negative income, which are less than one-half of one percent of households.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Because means-tested transfers and the federal tax system are progressive, income after transfers and taxes was less skewed than income before transfers and taxes. Among households in the lowest quintile, average income after transfers and taxes was about 64 percent higher than income before transfers and taxes in 2019—$38,900 versus $23,800 (see Exhibit 1). Average income after transfers and taxes in the middle quintile was $74,800. Because, overall, households in the middle quintile paid more in federal taxes than they received in means-tested transfers, average income after transfers and taxes for that quintile was about $7,000 less than the average income before transfers and taxes for the group.

Among households in the highest quintile, average income after transfers and taxes was about $252,100 in 2019. Because households at the top of the income distribution paid significantly more in federal taxes than they received in means-tested transfers, income after transfers and taxes for that quintile was about $80,000 less than the group’s income before transfers and taxes, on average. Among households in the top 1 percent of the income distribution, income after transfers and taxes was $1.4 million, on average—about $600,000 less than that group’s income before transfers and taxes. The average income after transfers and taxes for the top 0.01 percent was $30.0 million in 2019, or $13.0 million less than that group’s average income before transfers and taxes.

Exhibit 18.

Trends in the Distribution of Income After Transfers and Taxes, 1979 to 2019

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

All dollar amounts are expressed in 2019 dollars.

To calculate growth rates, CBO first converted all dollar amounts to 2019 dollars using the Bureau of Economic Analysis’s price index for personal consumption expenditures.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Over the 41-year period, all five quintiles reached their highest average income after transfers and taxes in 2019. Over the same period, income after transfers and taxes grew fastest among households at the top of the income distribution. However, it grew more evenly across the distribution than income before transfers and taxes because of the progressivity of the transfer and tax systems.

For the lower four quintiles, average federal tax rates fell over time, and average means-tested transfer rates increased. As a result, the average income after transfers and taxes grew more quickly than the average income before transfers and taxes for those income groups. The lowest quintile’s average income after transfers and taxes grew by a cumulative 94 percent (or at an average annual rate of 1.7 percent) between 1979 and 2019, and its average income before transfers and taxes grew by 45 percent. Similarly, the middle three quintiles’ average income after transfers and taxes grew by a cumulative 59 percent (or at an average annual rate of 1.2 percent) over that period, and their income before transfers and taxes grew by 43 percent.

The average federal tax rate for the highest quintile declined over time, so income after transfers and taxes grew slightly more quickly than income before transfers and taxes. That group’s income after transfers and taxes grew by a cumulative 123 percent (or at an average annual rate of 2.0 percent), rising from an average of $113,100 in 1979 to $252,100 in 2019. In comparison, the highest quintile’s income before transfers and taxes grew by 114 percent.

Exhibit 19.

Cumulative Growth in Income After Transfers and Taxes Among Households in the Highest Quintile, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

To calculate growth rates, CBO first converted all dollar amounts to 2019 dollars using the Bureau of Economic Analysis’s price index for personal consumption expenditures.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Between 1979 and 2019, income after transfers and taxes grew most quickly among households in the top 0.01 percent of the distribution, spurred by strong growth in income before transfers and taxes and a reduction in average tax rates. From 1979 to 2019, average income after transfers and taxes grew by the following amounts:

- 97 percent among households in the 81st to 99th percentiles, or at an average annual rate of 1.7 percent per year, from $98,200 to $193,700;

- 193 percent among households in the 99th to 99.9th percentiles, or at an average annual rate of 2.7 percent per year, from $284,300 to $833,000;

- 367 percent among households in the 99.9th to 99.99th percentiles, or at an average annual rate of 3.9 percent, from $838,300 to $3.9 million; and

- 507 percent among households in the top 0.01 percent of the distribution, or at an average annual rate of 4.6 percent, from $4.9 million to $30.0 million.

Because of reductions in the average federal tax rate over the 1979–2019 period, the growth of income after transfers and taxes surpassed the growth of income before transfers and taxes by 83 percentage points among households in the top 0.01 percent of the income distribution and by 46 percentage points among households in the 99.9th to 99.99th percentiles. In contrast, among households in the 81st to 99th percentiles and the 99th to 99.9th percentiles, income after transfers and taxes grew at roughly the same rate as income before transfers and taxes.

Exhibit 20.

Shares of Income After Transfers and Taxes, 1979 to 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shares do not add up to 100 percent because households with negative income are not shown.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Between 1979 and 2019, households in the top 1 percent of the income distribution received an increasing share of income after transfers and taxes, amounting to a gain of 6 percentage points. The middle three quintiles’ shares of income after transfers and taxes, in contrast, decreased by 5 percentage points over the period.

In 1979, the middle three quintiles received more than half of all income after transfers and taxes: 51 percent. By 2019, that share had declined to 45 percent. Meanwhile, the top 1 percent’s share of income after transfers and taxes rose from 7 percent in 1979 to 13 percent in 2019. Shares of income for the lowest quintile and the remainder of the highest quintile were comparatively constant over the period: The lowest quintile’s share fell by 0.1 percentage point, and the 81st to 99th percentiles’ share grew by 1 percentage point.

Because the share of federal taxes increased between 1979 and 2019 for households in the top 1 percent (see Exhibit 16), that group’s share of income after transfers and taxes grew more slowly than its share of income before transfers and taxes: The latter increased by 7 percentage points over the period versus a 6 percentage-point increase in the share of income after transfers and taxes. The group’s share of income after transfers and taxes fluctuated over the 41-year period in response to economic conditions and shifts in tax and transfer policies, peaking in 2007 at 17 percent.

Exhibit 21.

Shares of Income Before and After Transfers and Taxes, 2019

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shares do not add up to 100 percent because households with negative income are not shown.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

In 2019, income after transfers and taxes was more evenly distributed than income before transfers and taxes.

Households in the lower three quintiles received a larger share of income after transfers and taxes than of income before transfers and taxes in 2019. The lowest quintile received 8 percent of income after transfers and taxes, compared with 4 percent of income before transfers and taxes. The middle quintile’s share of income after transfers and taxes was 15 percent, and its share of income before transfers and taxes was 14 percent. Because households in the lower two quintiles received more in means-tested transfers than they paid in taxes, the transfer and tax systems combined to increase their shares of income.

In contrast, the share of income after transfers and taxes for the highest quintile was about 6 percentage points less than the share of income before transfers and taxes. Because those households paid more in taxes than they received in transfers, the transfer and tax systems combined to reduce their share of income from 55 percent to 48 percent. Much of that decline was experienced by households in the top 1 percent of the distribution, whose share of income after transfers and taxes was 13 percent, 3 percentage points lower than their share of income before transfers and taxes.

Income Inequality

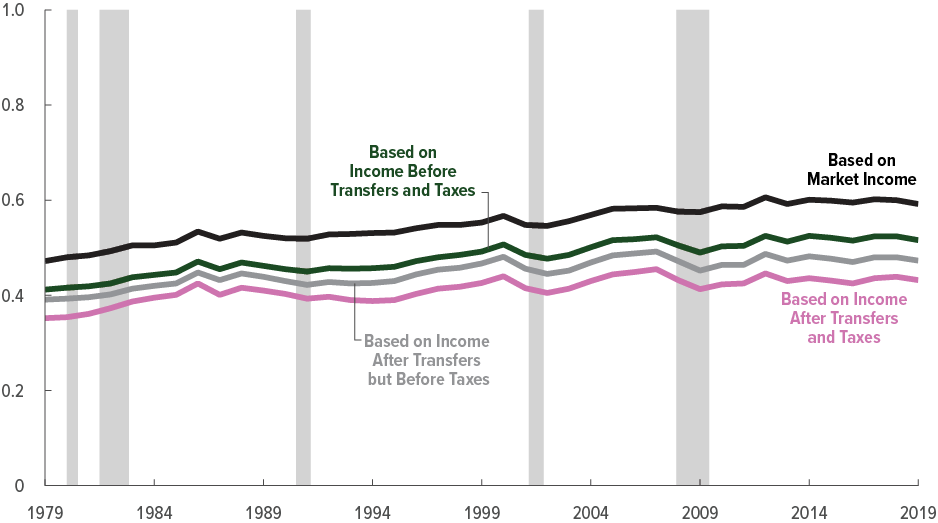

As the distribution of income shifted in the United States between 1979 and 2019, so did the degree of income inequality.17 A standard measure of income inequality is the Gini coefficient, which summarizes an entire distribution in a single number that ranges from zero to one. At the theoretical extremes, a value of zero means that income is distributed equally among all income groups, whereas a value of one indicates that all income is received by the highest income group, and none is received by any of the lower income groups.

The Gini coefficient can also be interpreted as a measure of one-half of the average difference in income between every pair of households in the population, divided by the average income of the total population. For example, the Gini coefficient based on income before transfers and taxes—which was 0.516 in 2019—indicates that the average difference in income before transfers and taxes between pairs of households in that year was equal to 103.2 percent (twice 0.516) of average household income, or about $80,800 (adjusted to account for differences in household size).

CBO’s analysis compares Gini coefficients based on four different income measures: market income, income before transfers and taxes, income after transfers but before taxes, and income after transfers and taxes. Social insurance benefits, transfers, and taxes tend to reduce income inequality as measured by the Gini coefficient. Still, the Gini coefficients based on each of the four income measures indicate a rise in income inequality between 1979 and 2019; changes in the distribution of market income caused much of that increase.

The degree to which means-tested transfers and federal taxes reduce income inequality can be measured by the difference between the Gini coefficient for income before transfers and taxes and the Gini coefficient for income after transfers and taxes. That difference has fluctuated over time, as average federal tax rates and means-tested transfer rates have changed. But overall, the degree to which income inequality was reduced by transfers and taxes increased between 1979 and 2019.

Exhibit 22.

Income Inequality As Measured by the Gini Coefficient, 1979 to 2019

Gini Coefficient

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

The Gini coefficient is a measure of income inequality that ranges from zero (the most equal distribution of income) to one (the least equal distribution of income).

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

Between 1979 and 2019, income inequality as measured by the Gini coefficient for all four income measures rose. Increases in market income at the top of the distribution drove much of the rise in income inequality over that time. Of the four measures of income presented here, income inequality as measured by market income is the highest. Social insurance benefits, particularly Social Security and Medicare benefits, reduced income inequality relative to market income inequality. (Those benefits are included in income before transfers and taxes.) The progressive structures of means-tested transfers and federal taxes also reduced income inequality, but by smaller amounts than social insurance benefits did.

During periods of economic expansion, such as the mid-1990s and mid-2000s, income inequality tended to increase. While income grew for all groups, including those at the bottom of the distribution, inequality increased because income at the top grew more.

There were also several temporary drops in income inequality over the years. Some drops, such as that in 2008, were largely attributable to economic recessions that brought about significant capital income losses—and, to a lesser extent, labor income losses—at the top of the income distribution. Other drops, including the decline in 2013, followed changes in tax laws that probably caused some high-income households to shift the realization of capital gains into the prior year.

Exhibit 23.

Reduction in Income Inequality Stemming From Means-Tested Transfers and Federal Taxes, 1979 to 2019

Change in Gini Coefficient

Data source: Congressional Budget Office. See www.cbo.gov/publication/58353#data.

Shaded vertical bars indicate the duration of recessions. (A recession extends from the peak of a business cycle to its trough.)

To measure the effect of means-tested transfers and federal taxes on inequality in each year, CBO subtracted the Gini coefficient for income before transfers and taxes from the Gini coefficient for income after transfers and taxes. A Gini coefficient value of zero indicates complete equality, and a value of one indicates complete inequality; thus, a negative change in the Gini coefficient indicates that inequality was reduced. The more negative the change, the greater the reduction in inequality.

For information about the methods underlying this analysis, see Appendix A. For detailed definitions of income measures, see Appendix B.

The Gini coefficient for income after transfers and taxes is lower than the coefficient for income before transfers and taxes because means-tested transfers and federal taxes in the United States are progressive. Although the degree to which transfers and federal taxes reduce income inequality varies from year to year, the extent to which they have done so has increased since 1979.

In 2019, the Gini coefficient for income after transfers and taxes was 0.432—that is, 0.084 less than the Gini coefficient was for income before transfers and taxes (see Exhibit 22). That reduction in inequality was larger than in 1979, when transfers and federal taxes reduced the Gini coefficient by 0.060, from 0.412 to 0.352.

The reduction in inequality as a result of taxes increased in the early 1990s, after lawmakers expanded the earned income tax credit and raised top individual marginal tax rates. It increased again after higher individual income tax rates went into effect in 2013, particularly for households at the top of the income distribution.

Similarly, means-tested transfers increasingly lessened income inequality when transfer rates grew among households in the lowest quintile. Major expansions in transfer rates occurred in the early 1990s, during the 2007–2009 recession, and in 2014 after Medicaid expanded under the Affordable Care Act.

1. In this report, CBO estimates that 315 million people lived in those households. The agency’s estimate of the U.S. population excludes members of the armed forces on active duty and people in institutions such as prisons or nursing homes.

2. Each quintile of the income distribution contains approximately the same number of people but slightly different numbers of households.

3. Market income comprises labor income (including cash wages, employers’ contributions for health insurance premiums, and payroll taxes paid by employers), business income, capital income (including realized capital gains), and income from other nongovernmental sources.

4. Although data from tax returns include information on tax filers’ family structure and age, they do not include information about people’s race, ethnicity, or education. The supplemental data posted along with this report include additional distributional data for three types of households: households headed by elderly people; households with children; and nonelderly, childless households. The additional data, broken out by household type, are reported for each income group. The supplemental data are available at www.cbo.gov/publication/58353#data.

5. Annual income is only one measure of economic well-being. In this report, CBO does not assess trends in the distributions of other measures of economic well-being, such as household income measured over a longer period, household consumption, or household wealth. Nor does this report analyze the considerable variation in income, taxes paid, and tax rates within each income group, which cannot be captured by calculating averages alone.

6. Much research has been conducted on the related topic of economic mobility. For a comprehensive overview of that research, see Federal Reserve Bank of St. Louis and the Board of Governors of the Federal Reserve System, Economic Mobility: Research and Ideas on Strengthening Families, Communities, and the Economy (2016), https://tinyurl.com/ycykrhbv. See also Katharine Bradbury, Family Characteristics and Macroeconomic Factors in U.S. Intragenerational Family Income Mobility, 1978–2014, Opportunity and Inclusive Growth Institute System Working Paper 19-08 (Federal Reserve Bank of Minneapolis, October 2019), https://tinyurl.com/y2wrztu6 (PDF).

7. In addition to the federal government’s fiscal (tax and spending) policies, its monetary, regulatory, and trade policies affect the distribution of household income. The direct distributional effects of those other federal policies, however, are not examined in this report. Although some state-level means-tested transfers are included in this analysis, most state and local fiscal policies are also not examined here.

8. In this analysis, CBO classified means-tested transfers in four categories: Medicaid and the Children’s Health Insurance Program, the Supplemental Nutrition Assistance Program, Supplemental Security Income, and other means-tested transfers. The other means-tested transfers that are analyzed in this report are housing assistance programs, low-income subsidies for Part D of Medicare (which covers prescription drugs), Temporary Assistance for Needy Families, child nutrition programs, cost-sharing reductions under the Affordable Care Act, the Low Income Home Energy Assistance Program, and state and local government general assistance programs.

9. Although means-tested transfers are designed to assist people with low income, the data indicate that some high-income households receive benefits from the transfer programs. That may happen for several reasons. For example, some people have income that varies during the year and may therefore qualify for benefits on the basis of low monthly income even though their annual income is high. In addition, some people who qualify for benefits because their own income is low live in high-income households. Finally, a portion of the benefits reported as going to higher-income households probably reflects some misreporting of income, program participation, and benefit amounts in the survey data that underlie CBO’s estimates.

10. CBO’s estimates represent the number of recipients who were ever enrolled in Medicaid or CHIP in a given calendar year. Furthermore, the estimates apply to the noninstitutionalized population; they do not include recipients living in nursing homes and other long-term care facilities. The CHIP program began in 1998.

11. The value of Medicaid and CHIP benefits allocated to households is based on the average cost to the government of providing those benefits. CBO did not attempt to estimate the value that households place on those benefits. Although sick people enrolled in federal health programs that provide assistance to low-income families may value those benefits more than the average cost to the government of providing them, some empirical evidence suggests that, on average, Medicaid recipients value the benefits at less than the average cost to the government of providing those benefits. See Amy Finkelstein, Nathaniel Hendren, and Erzo F. P. Luttmer, “The Value of Medicaid: Interpreting Results From the Oregon Health Insurance Experiment,” Journal of Political Economy, vol. 127, no. 6 (December 2019), pp. 2836–2874, https://tinyurl.com/3ks7wzdt.

12. The remaining federal revenue sources not allocated to U.S. households include states’ deposits for unemployment insurance, estate and gift taxes, net income earned by the Federal Reserve System, customs duties, and miscellaneous fees and fines. Because of the complexity of estimating state and local taxes for individual households, this report considers federal taxes only. Researchers differ about whether state and local taxes are, on net, regressive, proportional, or slightly progressive, but most agree that state and local taxes are less progressive than federal taxes. For estimates of the distribution of state and local taxes, see Meg Wiehe and others, Who Pays? A Distributional Analysis of the Tax Systems in All 50 States, 6th ed. (Institute on Taxation and Economic Policy, October 2018), https://itep.org/whopays/; and Gerald Prante and Scott Hodge, The Distribution of Tax and Spending Policies in the United States, Special Report 211 (Tax Foundation, November 2013), https://tinyurl.com/roj9t2g (PDF).

13. Federal taxes allocated to households in this analysis are based on tax liabilities incurred in calendar year 2019.

14. For information about the distribution of tax expenditures in 2019, see Congressional Budget Office, The Distribution of Major Tax Expenditures in 2019 (October 2021), www.cbo.gov/publication/57413.